ECSDA releases 2013 CSD Factbook

2 Sept 2014 – This year’s edition offers an up-to-date overview of the CSD landscape in Europe.

The value of securities held on CSD accounts increased by more than 6% in 2013

From 2012 to 2013, the total value of all securities held at ECSDA members increased by 6.5% to reach almost EUR 48 trillion. This increase adds to the generally positive trend since 2010.

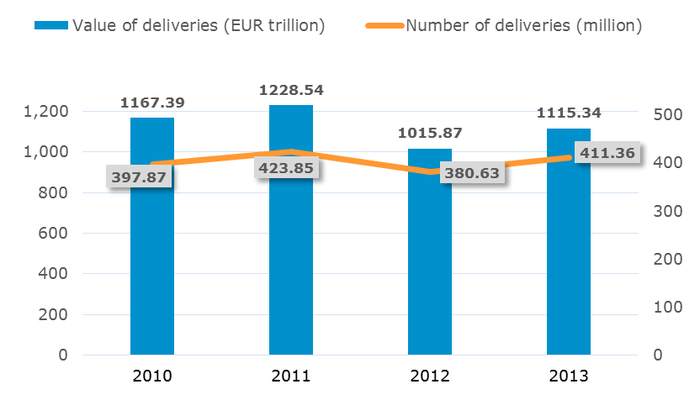

Over the year, European CSDs collectively processed around 410 million delivery instructions, 30 million more than in 2012. In terms of value, these delivery instructions represented over EUR 1.1 quadrillion, well above last year’s settlement volumes but still below the peak in 2011:

CSD broaden the array of financial instruments accepted for settlement

All European CSDs settle equities and the overwhelming majority settle corporate bonds and government securities. Besides, more than 80% of CSDs have developed services for mutual funds, not only limited to settlement but also including order routing and valuation services. Other instruments accepted for settlement include Depository Receipts, cooperative share units, asset backed securities, structured products, and in a few cases greenhouse gas emission certificates.

An extended role as providers of reference data

80% of European CSDs act as national numbering agencies and thus allocate ISIN codes to newly issued securities. Furthermore, 5 CSDs were recently authorised to allocate Legal Entity Identifiers (LEI) to financial counterparties in the market(s) in which they operate.

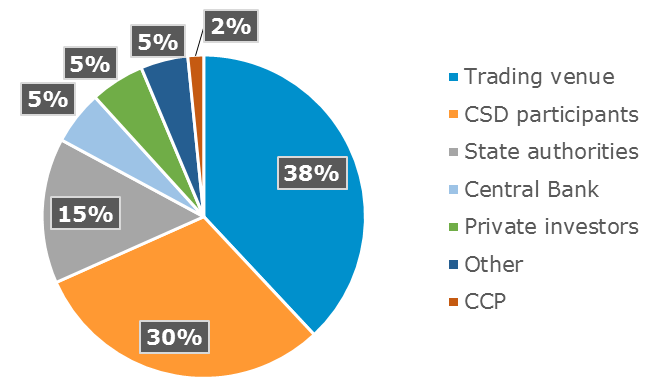

CSD ownership models remain very diverse

In the EU, stock exchanges represent the main shareholder category for CSDs, whereas other European CSDs outside the EU are characterised by a stronger involvement of the State in the CSD capital. In both EU and non-EU CSDs, CSD participants represent on average close to a third of CSD owners. The following pie chart shows the proportion of shareholders from different categories in a theoretical CSD based on the ownership structure of the 41 ECSDA members:

An international client base

CSD participants are typically wholesale financial firms. Leaving the two ICSDs aside (since by nature they do not operate in a domestic environment), European CSDs had on average 23% of non-domestic participants in 2013. That said, the rate tends to be much higher in countries with a high degree of regional integration (e.g. Benelux, Nordics).

59% of European CSDs maintain end investor accounts in their books, although not all of them operate a pure direct holding model. As a result of different market practices as regards account holding structures, the number of securities accounts maintained by a CSD varies considerably from country to country (from less than 1,000 accounts to more than 10 million).

Other interesting facts on European CSDs:

- With the exception of Ireland, all EU countries have a CSD operating on their territory. Belgium even hosts 4 CSDs (including one operated by the central bank), and Luxembourg 3.

- EU CSDs are now also regulated by the CSD Regulation, which will enter into force on 17 September 2014. All CSDs are already subject to the international oversight Principles of CPSS and IOSCO.

- 6 ECSDA members operate with a banking license and are therefore also subject to the relevant banking laws.

- The vast majority of European CSDs (90%) operates an RTGS or “real-time gross settlement” model. Other settlement models involve some form of netting, for cash and/or securities, and are typically used for on-exchange transactions.

- ECSDA members collectively employ more than 7,800 people, among which 82% are employed by EU-based CSDs. Excluding the two ICSDs, the average European CSD has slightly more than 100 employees