The registration of securities holders

19 Jul 2016 – The registration of securities holders refers to the process of recording ownership or legal holding in securities in an official list called the register. This list facilitates the identification of securities holders by issuers and regulators. A new report by ECSDA looks at existing legal requirements in 38 European markets, highlighting the current lack of harmonisation in the legal and practical approaches to securities holders registration.

Here are some of the key findings:

- Registration grants a certain level of legal protection to securities holders

The recording of securities holdings in the register has legal effects. Although these differ across markets, registration typically means that the investor’s rights over the securities are enforceable towards the issuer, such as the right to receive a dividend or interest payment.

- Shares are more frequently subject to registration requirements than bonds

Registration requirements are generally associated with the holding of shares because companies have a strong interest in being able to identify their shareholders. Unlike bondholders, shareholders have a say in the way the company is managed, and hold voting rights at General Meetings. Registration is therefore mandatory for shares in roughly half of the markets surveyed, whereas it is only mandatory for debt instruments in around 1/3 of the markets.

Bearer securities, which do not require the maintenance of a register, are still commonplace. Bearer shares outnumber registered shares in 8 markets, while debt instruments are primarily held in bearer form in 14 markets. Although international securities like eurobonds are not included in this report, they are also primarily held in bearer form. The below chart shows the proportion of registered securities across European markets, based on the market value of all of securities held at the CSD:

- The link between registration and settlement varies across markets

The relation between registration and settlement is not the same in every market. Where beneficial owner accounts are maintained at the CSD, the register tends to be a direct reflection of CSD accounts, which means that the register is updated on a daily (or even intraday) basis to reflect the changes in CSD records following a securities transfer between accounts at the CSD. In other markets, the register is maintained separately from CSD accounts and may only be updated on an ad hoc basis, typically at the request of the issuer.

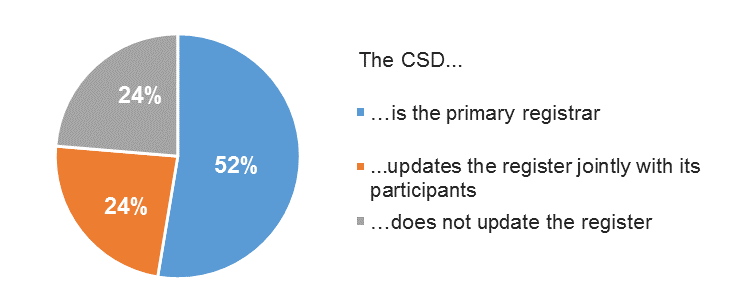

- CSDs are not always involved in the maintenance of the register

Issuers are responsible for maintaining the list of their registered securities holders, but, in practice, they frequently outsource this task to a third party entity. The third party can be a CSD, an intermediary, or any other entity authorised to act as registrar.

In more than half of European markets, the CSD acts as the sole or primary registrar, as illustrated in the following chart:

In other cases, either the CSD updates the register jointly with its participants (banks maintaining accounts on behalf of investors), or it does not play any direct role in updating the register.

In 71% of the markets surveyed, irrespective of whether the CSD is involved, the register is updated on an ongoing basis, i.e. at least daily. In the remaining markets, the register is only updated on an ad hoc basis, typically at the request of the issuer prior to a General Meeting or another corporate event.

- The information items contained in the register are not harmonised

The format and details of the records stored in the securities register vary. Most registers include at a minimum the name of the securities holders, an address and the relevant securities balances. Other information items, such as an identification number or the nationality of the investor, are only required in certain countries. The chart below illustrates the information items which are legally required in the register of securities holders across 38 European markets:

It important to remember, however, that in the majority of European markets, the names on the register do not necessarily correspond to the names of end investors since securities can be held in “nominee” accounts, i.e. the legal holder of the securities is the intermediary maintaining securities accounts on behalf of the end investor, rather than the end investor him- or herself.

To find out more, read the full ECSDA report on the registration of securities holders.